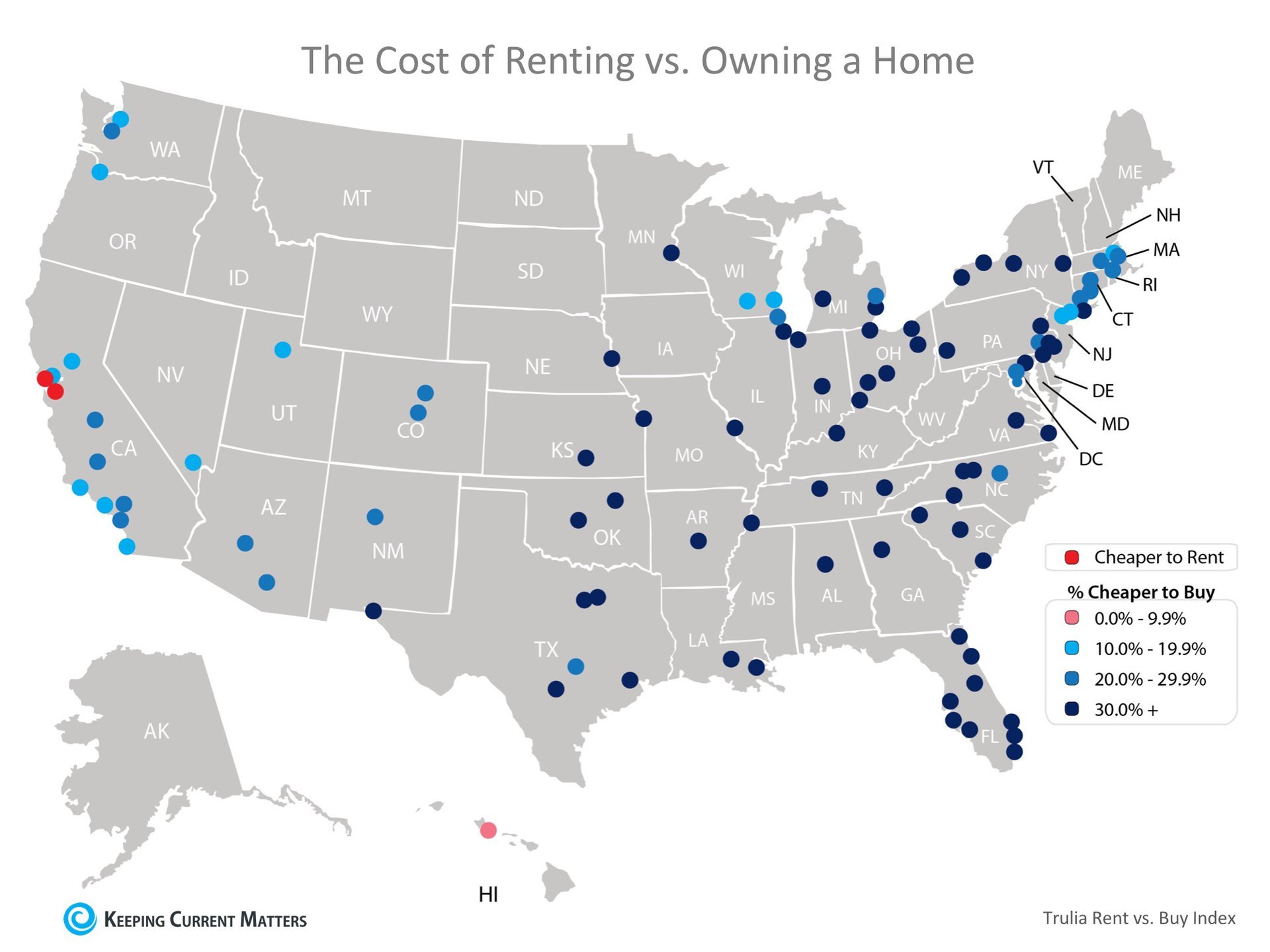

In the six years that Trulia has conducted this study, this is the first time that it was cheaper to rent than buy in any of the metropolitan areas.

It’s no surprise, however, that those two metros are San Jose and San Francisco, CA, where median home prices have jumped to over $1 million dollars this year. Home values in San Jose have risen 29% in the last year, while rents have remained relatively unchanged.

For the 98 metros where homeownership wins out, 97 of them show a double-digit advantage when buying. The range is an average of 2.0% less expensive in Honolulu (HI), all the way up to 48.9% in Detroit (MI), and 26.3% nationwide!

Below is a map of the 100 metros that were studied. The darker the blue dot on the metro, the cheaper it is to buy there.

In order to calculate the true cost of renting vs. buying, Trulia includes all assumed renting costs, including one-time costs (like security deposits), and compares them to the monthly costs of owning a home (insurance, mortgage payments, taxes, and maintenance) including one-time costs (down payments, closing costs, sale proceeds). They also assume that households stay in their home for seven years, put down a 20% down payment, and take out a 30-year fixed rate mortgage. The full methodology is included with the study results here.

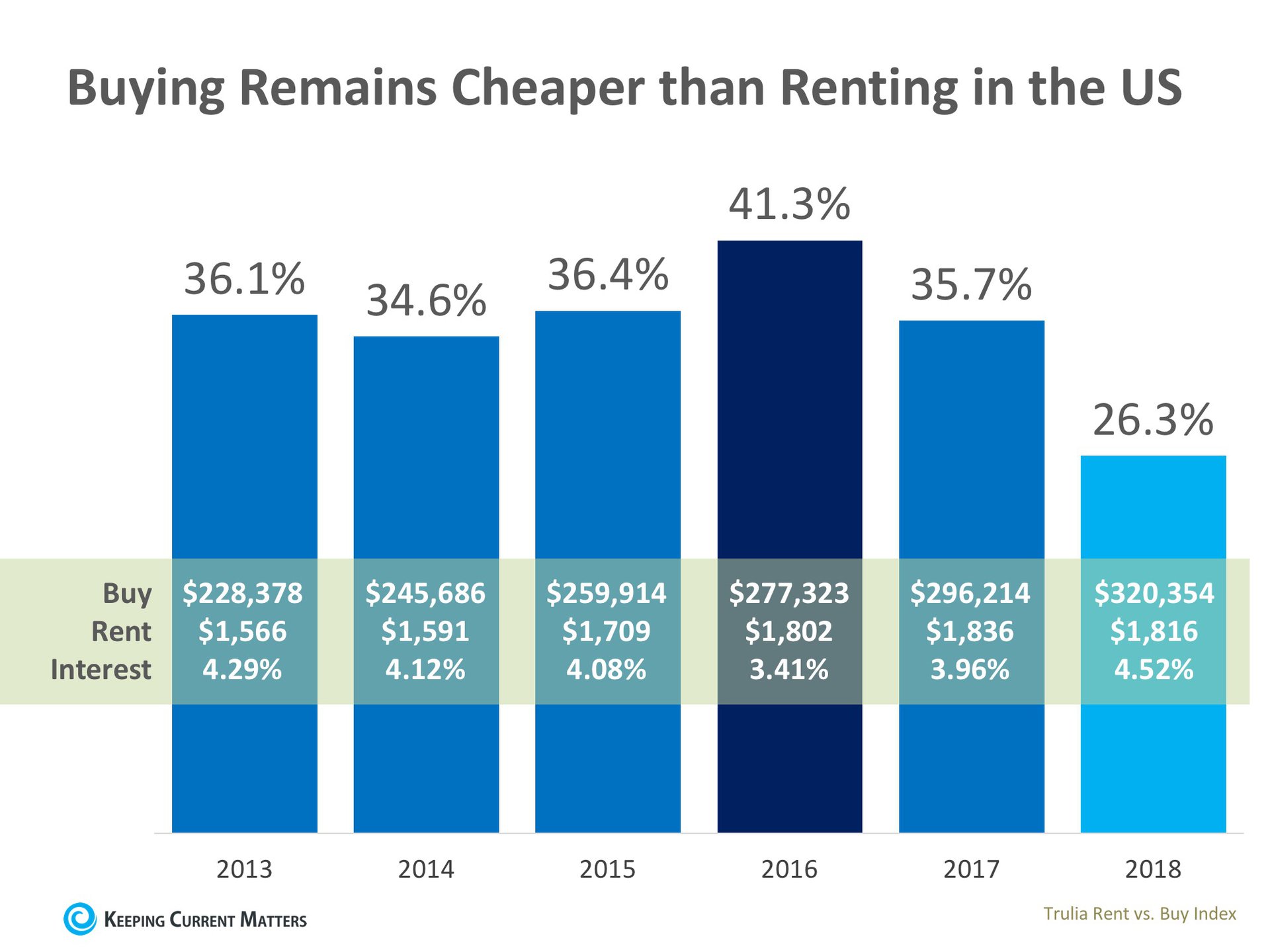

Below is a chart created with the data from the last six years of the study, showing the impact of the median home price, rental price, and 30-year fixed rate interest rate used to calculate the ‘cheaper to buy’ metric.

In 2016, when buying was 41.3% less expensive than renting, the average mortgage rate was the driving force behind the difference. Rates this year are the highest they have been in six years which has narrowed the gap, all while home price appreciation has also been driven up by a lack of homes for sale.

Cheryl Young, Trulia’s Chief Economist, had this to say,

“One point deserves emphasizing: The ultra-costly San Francisco Bay Area is not a harbinger for the nation as a whole. While renting may outweigh buying in San Jose and San Francisco, it is unlikely that renting will tip the scales nationally anytime soon.”

Bottom Line

Homeownership provides many benefits beyond the financial ones. If you are one of the many renters out there who would like to evaluate your ability to buy this year, meet with a local real estate professional who can help you find your dream home.

]]>This is a big problem, says Martin Choy, operations manager at Westwood Mortgage in Seattle.

“Most homeowners should know what their rate is. If they have an adjustable rate mortgage [ARM], then they should contact their lender immediately and get their current rate,” Choy says.

Rates Are Climbing, so Borrowers Should Act Now

As rates continue to rise, this could be your last chance for many years to lock in a lower rate.

“During the big boom, before this last election, we could refinance mortgages at no cost because the rates were so low, but now the rates are heading up,” Choy says.

The average rates on 30-, 15- and 10-year fixed refinances have risen from a year ago, according to Bankrate’s weekly survey of large lenders. The benchmark 30-year fixed-rate mortgage rose to 4.70 percent (as of July 11, 2018) from 4.13 percent a year earlier.

A $200,000 mortgage with a 4.70 percent interest rate costs $119 a month more in interest than the same mortgage with a 4.13 percent rate. As rates and mortgage amounts go up, the impact on your bottom line increases. Over time, this difference in rates can cost you thousands of dollars.

Good Candidates for Refinancing

When you refinance your mortgage, you pay off the remaining balance on your current loan and get a new one. You can get a new rate, new terms, or a new rate and new terms. You can get a cash-out refinance where you tap into the equity to extract cash and then get a new mortgage. You can even pay money in and take out a smaller mortgage.

Those with adjustable-rate mortgages may be good candidates for refinancing. As mortgage rates climb, so will your monthly payments. If you lock in a fixed-rate mortgage now, you may be able to save thousands of dollars later.

The same is true for people with high-rate mortgages who have since improved their credit.

“There are many variables in determining whether refinancing is a good option,” says Choy. “How much do you owe? How much is your house appraised for? Is your credit score good? If you’re in better financial shape now, both with your monthly debt ratio and credit score than when you got your mortgage, then you could qualify for better rates.”

Today, most people aren’t getting ARMs because the rates are about the same as fixed-rate mortgages, says Choy.

“It’s always better to get a fixed-rate loan than an ARM when interest rates are equal. Now is a good time to refinance an ARM before rates get even higher.”

Cash-Out Refinance Options

If you have outstanding higher-rate consumer debt and an above-market mortgage interest rate, a cash-out refinance might be a good option. That way you can consolidate all the debt into one presumably more affordable monthly payment.

Not only are mortgage rates rising; so are interest rates for credit card debt. Because credit card interest rates follow in lockstep with mortgage rates, people with credit card debt might be looking at higher monthly payments.

“With a cash-out refi, you can use that money to pay off debt and get a new mortgage with better rates. That is an option for some homeowners,” says Choy.

What Does Refinancing Cost?

Refinancing fees vary by lender and state, so be sure to shop around for specific costs. Bankrate’s mortgage rate tables are a good place to start looking at rates in your area. Calculate when you’ll break even on the new mortgage by taking into account the costs of refinancing and any prepayment penalty for paying off your mortgage early.

On average, borrowers can expect to pay between 3 and 6 percent of their balance in refinancing fees. Costs might include:

- Application fee: This charge varies by lender and is used to cover processing your application and credit report. The cost ranges from $75-$300.

- Loan origination fee: The lender charges this fee for preparing your loan. This may be between 0 percent and 1.5 percent of the loan principal.

- Points: You might pay loan-discount points, which is a one-time fee for reducing the interest rate on your loan. Each point is equal to 1 percent of the amount of your mortgage. There is another point-based fee charged by lenders to earn money on the loan. This latter fee of up to 3 percent of the loan principal can sometimes be negotiated.

Other fees might include:

- Appraisal fee

- Title search/title insurance

- FHA, RDS or VA fees or PMI

- Homeowner’s insurance

- Attorney review

- Inspection

- Surveys

Sometimes these fees can be rolled into your new mortgage, or the lender will pay them in exchange for a higher interest rate. Refinances that don’t require borrowers to pay these up-front fees are known as “no-cost” refinancing.

]]>